The controversy surrounding Peter Navarro’s comment, branding the Ukraine conflict as “Modi’s war” has escalated into one of the most critical episodes in recent U.S.–India relations. At its heart lies a question bigger than crude oil: can India chart an independent course in global energy markets and foreign policy, or must it conform to the strategic demands of its Western partners? The answer will not only define India’s economic resilience but also its position in a deeply polarized world order.

The Provocation and Its Meaning

Peter Navarro, a senior trade adviser to former U.S. President Donald Trump, set off the storm by alleging that India’s continued imports of Russian crude are “prolonging the war in Ukraine.” His phrase “Modi’s war” was a deliberate rhetorical strike, designed to pin responsibility for Moscow’s resilience not just on the Kremlin but also on New Delhi. According to Navarro, every barrel of oil India buys from Russia keeps the Russian treasury flush with dollars, indirectly underwriting tanks, missiles, and salaries of soldiers on the Ukrainian front. The accusation is extraordinary in its bluntness. Never before has a U.S. official of such senior rank equated India’s energy strategy with active complicity in a European conflict. For Washington, this framing is also tactical: it provides political cover for sweeping tariffs on Indian exports by presenting them as a moral necessity rather than a commercial dispute.

Tariffs as Punishment

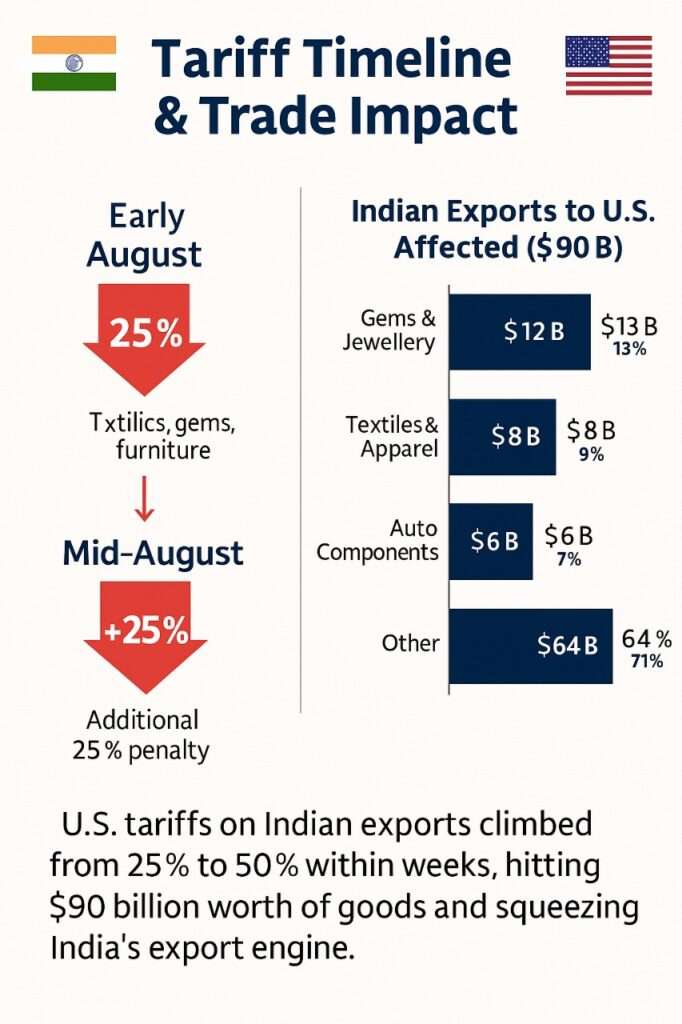

The policy consequences were swift. In August 2025, the United States imposed a cumulative 50 per cent tariff on Indian exports. This comprised an initial 25 per cent duty on textiles, gems, and auto components, followed by an additional 25 per cent penalty specifically tied to India’s continued oil and defense purchases from Russia. Together, these measures hit nearly $90 billion worth of Indian exports annually.

For India’s economy, already navigating global headwinds, the impact is severe. Gems and jewellery, India’s largest export category to the U.S. at nearly $12 billion a year face immediate losses. Small and medium enterprises, particularly in textiles and handicrafts, see their competitiveness erode overnight. On the American side, importers of Indian pharmaceuticals, IT services, and automotive components face higher costs, potentially fueling inflation. Navarro’s team has dangled a conditional reprieve: if India halts Russian crude imports, half the tariffs could be rolled back. Yet New Delhi has dismissed the offer, calling the linkage of trade and energy policy an “unprecedented violation of sovereignty.”

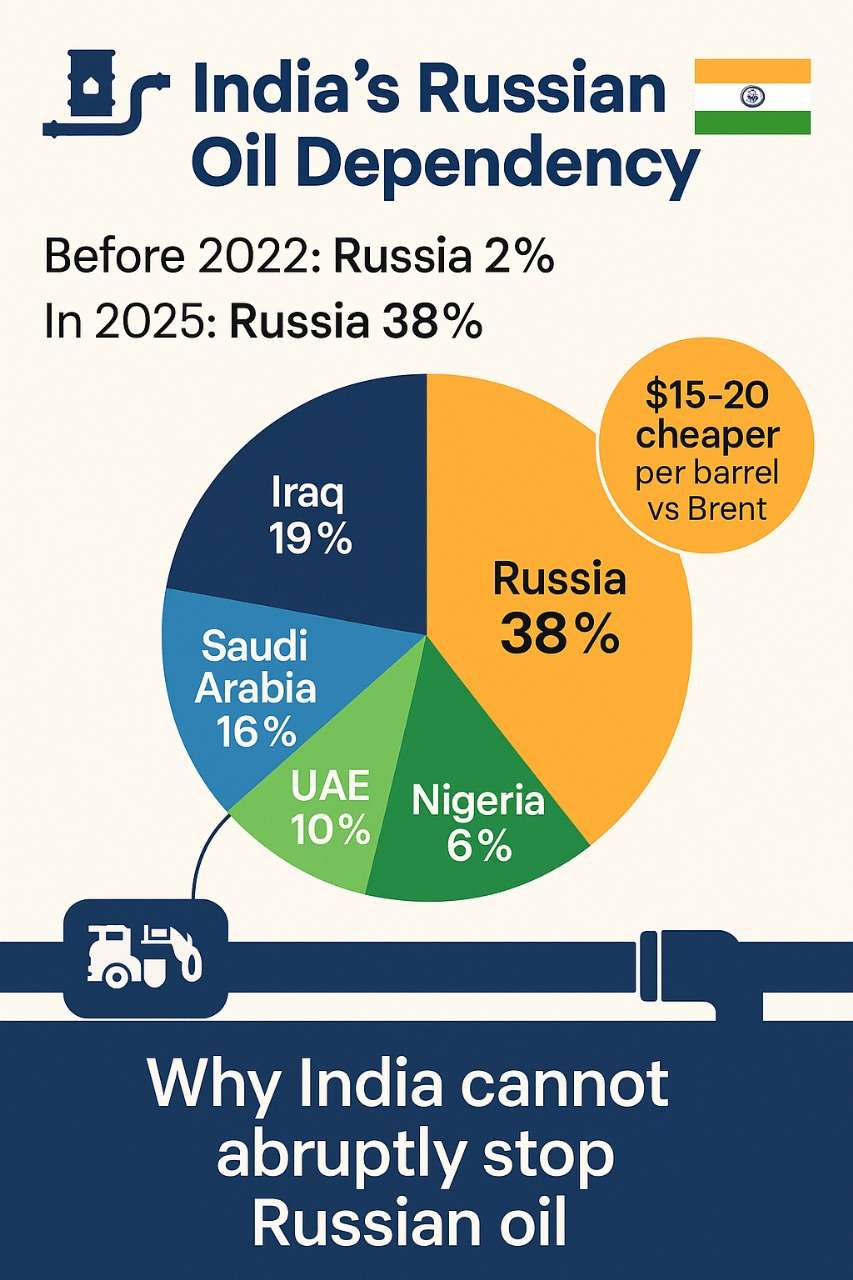

The depth of India’s reliance on Russian crude cannot be overstated. Before the Ukraine war, Russia accounted for barely 1–2 per cent of India’s oil imports. By 2024–25, that figure surged beyond 38 per cent, making Russia India’s single-largest supplier, ahead of Iraq and Saudi Arabia. The attraction is simple: discounts. Russian crude has consistently been priced $15–20 below Brent benchmark levels, allowing Indian refiners to save billions. These savings flow into domestic fuel prices, moderating inflation that otherwise could devastate household budgets. In the fiscal year 2024–25 alone, India saved an estimated $7–9 billion by opting for Russian barrels over Middle Eastern counterparts.

For a country where 85 per cent of oil is imported, abandoning such discounts is nearly impossible without triggering inflationary shocks. Petrol and diesel prices directly impact food transport, manufacturing costs, and even voter sentiment. As one Indian official remarked privately, “No government in New Delhi can survive politically if fuel prices spiral by 20 per cent to satisfy Washington.”

While Washington frames this as a moral issue punishing Moscow’s war machine; the geopolitical undertones are unmistakable. The United States expects its allies to fall in line with sanctions regimes. Yet India insists on strategic autonomy, arguing that it cannot mortgage its national interest to Western diktats.

India’s policymakers point to Western hypocrisy. Europe, while vocal about sanctions, continues to import Russian LNG, fertilizers, and nuclear components. The U.S. itself still buys Russian uranium. China, meanwhile, has dramatically ramped up its imports of Russian crude, surpassing 2.3 million barrels per day, dwarfing India’s intake. Yet no punitive tariffs are leveled against Beijing. From New Delhi’s vantage point, this asymmetry smacks of double standards, undermining the credibility of Washington’s pressure campaign.Moreover, India argues that it is not just a consumer but also a supplier to the West. Much of the Russian crude refined in Indian facilities is exported as gasoline, diesel, and jet fuel to Europe, Japan, and even the U.S. The paradox is glaring: Western consumers are burning fuel made from Russian crude, but India alone is scapegoated for the trade.

Questions That Must Be Asked

This standoff raises fundamental questions. Can India continue to buy discounted oil indefinitely without facing escalating sanctions? Will Russia remain a reliable supplier if its war costs deepen and domestic needs rise? For the United States, can it afford to alienate India, the very partner it has elevated as central to its Indo-Pacific strategy, while simultaneously contending with an assertive China? And for the global order, can sanctions maintain legitimacy if they are selectively applied?

These questions underscore the fragility of trust between Washington and New Delhi. The “Modi’s war” remark is not just a soundbite; it is a symptom of deeper fissures in expectations.

Economic and Political Consequences

The tariffs land at a politically sensitive moment for both countries. In India, where elections loom in 2026, rising energy prices and export losses could become potent opposition weapons. For the U.S., where Trump’s administration emphasizes reshoring and tough trade policy, India is portrayed as an opportunist rather than a partner.

Industry bodies in India warn of job losses in export-driven sectors. The Federation of Indian Export Organisations estimates that tariffs could shave 0.3–0.5 per cent off GDP growth if not reversed quickly. American companies too are uneasy; over $35 billion of annual imports from India sustain their supply chains. Rising costs could fuel inflation, eroding Trump’s claims of economic stewardship.

The Global Energy Puzzle

At the heart of the dispute lies the global oil market’s complexity. Russian crude no longer flows directly to Europe but instead routes to Asia; chiefly India and China, before being refined and shipped back as finished products. This circuitous trade highlights the porousness of sanctions regimes. Analysts argue that punishing India will not choke Russian revenues; it will simply redirect flows, potentially empowering China.

Additionally, OPEC+ dynamics complicate matters. Saudi Arabia and the UAE, though close U.S. allies, have not dramatically increased production to compensate for Russian supply. This leaves few alternatives for India. Meanwhile, renewables, though expanding rapidly, account for only about 10 per cent of India’s energy mix, far from displacing fossil fuels.

Forthcoming Angles

Several flashpoints loom. The European Union is reviewing its price-cap mechanism, which could further squeeze India’s Russian purchases after October 2025. Domestically, India may intensify efforts to diversify; tapping greater volumes from Iraq, Nigeria, and the U.S. itself, but these come at higher costs.

Diplomatically, the Trump-Modi meeting at the United Nations General Assembly in September could determine whether de-escalation is possible. If Washington doubles down, New Delhi may pivot more decisively toward BRICS partners, especially with China and Russia championing alternatives to the dollar-dominated oil trade.

India’s long-term play may involve accelerating its renewable ambitions under the 2070 Net-Zero pledge, but in the medium term, its dependence on affordable oil imports will remain unshakable.

Ultimately, this dispute is a crucible for India’s doctrine of strategic autonomy. Since independence, New Delhi has resisted alignment with any single bloc, preferring pragmatic partnerships across divides. Today, that doctrine is under stress: can India simultaneously deepen ties with Washington while defying its most urgent demand? Can it sustain its energy bargains with Moscow without jeopardizing access to Western markets and technology?

For Washington, the risk is equally stark. By coercing rather than persuading India, it may push its most important Asian partner toward alternative alignments, weakening the very Indo-Pacific strategy meant to contain China.

Peter Navarro’s incendiary phrase “Modi’s war” is more than political theatre. It crystallizes the collision between national interest and alliance expectations, between cheap oil and costly principles, between a multipolar world and the remnants of unipolar dominance. For India, the defense is clear: energy security for 1.4 billion people cannot be compromised. For the U.S., the argument is equally forceful: global sanctions mean little if major economies carve out exceptions.

As the standoff deepens, the outcome will shape not only bilateral trade but the future architecture of global geopolitics. Whether this is resolved through negotiation, confrontation, or quiet compromise, one fact is undeniable: oil has once again become the fuel not just of economies, but of diplomacy, strategy, and conflict narratives.